What is a Swap Rate?

What is a swap rate?

A forex swap rate, also known as a rollover rate or a swap, is a fee that is paid or charged to an open trade at the end of each trading session. It’s the interest fee, which is charged or earned, for keeping positions open overnight. A swap rate allows positions to be extended into the next interbank session without closing or settling.

How is a swap rate determined?

A swap or rollover rate is determined by the difference in interest rates between the countries involved in a currency pair. For example, if you are trading the Australian dollar against the United States dollar (AUD/USD), the rollover rate calculation would involve the interest rates between Australia and the United States. Whether the position is long or short, a swap rate is applied. Because of this, each currency pair has its own swap rate.

Swap rates can be calculated using the following formula:

Rollover rate = (Base currency interest rate – Quote currency interest rate) / (365 x Exchange Rate).

Calculating swap rates can be explored further here.

Types of swaps

There are several types of swaps in financial trading.

Interest rate swaps

An interest rate swap (IRS) is a derivative contract where two parties exchange interest payments on the underlying debt. The most common type of IRS involves the exchange of fixed-rate payments for variable-rate payments. An IRS allows companies and/or banks to hedge their exposure to interest rate changes.

Currency swaps

A currency swap is a contract where two parties trade principal and interest in one currency for the same in another currency. A currency swap is usually executed by a bank or financial institution to hedge exposure to exchange rates. Unlike an IRS, a currency swap involves the exchange of principal.

Commodity swaps

A commodity swap is a derivative contract where two parties agree to exchange cash flows based on the price of an underlying commodity, such as oil. The agreement involves a fixed-leg component and a variable-leg component, allowing traders to fix the price of an agreed quantity of the commodity, at a future date.

Credit default swaps

Also known as a CDS, a credit default swap is similar to an insurance policy. It is a contract that allows traders to swap or offset their credit risk with another trader or investor. For example, a trader may decide to invest in company bonds, in exchange for a fixed rate of interest, known as a bond dividend. To protect their investment against company default, the trader may engage in a CDS, usually issued by a bank or an insurance provider. The CFD seller then charges the trader a fee in exchange for taking on the risk.

Zero-coupon swaps

In financial trading, a zero-coupon swap is a linear interest rate derivative (IRD). It’s an exchange of cash flows where the variable-leg interest payments are made periodically, whereas the fixed-leg component is made as a lump sum at maturity.

Total return swaps

Also known as a TRS, a total return swap is a contract between two parties where one party makes payments based on a set rate, being fixed or variable. Whereas the second party makes repayments based on the return of an underlying asset.

Libor swap rate

LIBOR is an acronym for London Inter-Bank Offered Rate. It’s the benchmark for variable short-term interest rates used by high-credit banks. The rate is set daily and has seven different maturity dates, including one day, and one week. 1, 2, 3, 6 and 12 months.

What is the value of a swap?

At the initiation or start date of a swap, the value is zero to both parties involved. The value of the swap then changes over time as the value of the underlying asset or interest rate changes. Because one leg of the swap is fixed and the other leg is variable, any positive change for one party will result in an adverse change to the other party.

At the initiation date, the two parties involved in a swap will agree to exchange cash flows to the same value. Therefore, fixed value = variable value. The party making payments on a variable rate will typically use the benchmark rate set by LIBOR. The party making payments based on a fixed rate uses a benchmark to US Treasury Bonds.

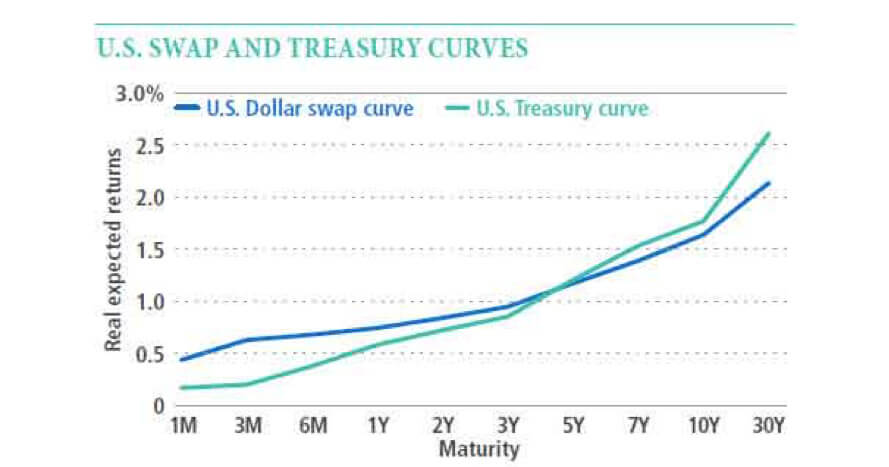

What is the swap rate curve?

It’s essentially a yield curve of any given swap. It shows traders the possible return of a swap over different maturity dates. A swap rate curve is illustrated by a chart that has the swap rate dotted along the y-axis (the vertical line) and maturity date plotted on the x-axis (the horizontal line). It’s also used as a benchmark for determining the funds rate. This is used to price fixed income products such as bonds. An example of a swap curve can be demonstrated on the below chart.

Practise trading the financial markets with Eightcap’s free demo account and gain exposure to a range of financial assets.